You own your car outright. You need a $5,000 loan. Your credit score is 560. A lender offers you two options: an unsecured loan at 28% APR, or a secured loan backed by your car title at 18% APR.

The secured rate looks better. Obviously. Ten percentage points is a lot of money over three years. But here's the question nobody walks you through: if something goes wrong, is the savings worth the risk of losing the vehicle that gets you to work?

That's not a yes-or-no answer. It's a math problem with a risk variable attached. Let me show you how to work through it.

The Rate Gap Is Real (But So Is the Risk)

Secured personal loans consistently offer lower rates than unsecured ones, even for borrowers with poor credit. According to NerdWallet, the average APR for bad credit borrowers (scores 300 to 629) who prequalified for personal loans in 2024 was 21.65%. Best Egg reports that their secured loan APRs average roughly 20% lower than their unsecured APRs for comparable borrowers. LendingTree shows secured personal loan rates as low as 8% to 15% for some bad credit borrowers, depending on the lender and collateral type.

Let's put dollar amounts on that gap.

A $5,000 unsecured loan at 28% APR over 36 months costs approximately $2,440 in total interest. Your monthly payment runs about $207.

The same $5,000 as a secured loan at 18% APR over 36 months costs approximately $1,500 in total interest. Your monthly payment drops to around $181.

That's $940 in savings and $26 less per month. Real money. Not theoretical. But that $940 only matters if you make every single payment. If you miss payments and the lender repossesses your car, the math inverts catastrophically.

What Counts as Collateral (It's Not Just Your Car)

When people hear "secured loan," they think car title. That's one option, but it's not the only one, and it's not always the smartest.

Vehicles

The most common collateral for bad credit secured personal loans. OneMain Financial accepts vehicles under 10 years old. Upgrade accepts cars up to 20 years old. You keep driving the car, but the lender places a lien on the title. If you default, they can repossess it.

Risk level: high. If you lose your car, you might lose your ability to earn income, which makes repaying any debt harder, not easier.

Savings Accounts and CDs

Some lenders and credit unions offer loans secured by a savings account or certificate of deposit. You deposit money (say, $1,000), the bank freezes those funds as collateral, and you borrow against them. First Tech Federal Credit Union offers savings-secured loans at 6.99% to 18% APR with no origination fee.

Risk level: low. The worst case is you lose access to the money in the account, which you already set aside for this purpose. Your car stays in your driveway. Your income stays intact.

Home Fixtures and Other Assets

Upgrade accepts built-in home fixtures like cabinets, ceiling fans, and light fixtures as collateral. This is less common and applies mainly to home improvement loans. The practical risk is low (nobody is going to repossess your ceiling fan), but it creates a secured loan structure that can improve your rate.

The takeaway: collateral exists on a spectrum. A CD sitting in a bank account is very different from the car you drive to work every morning. Where your collateral sits on that spectrum should shape your decision.

The Breakeven Math: When Collateral Saves You Money

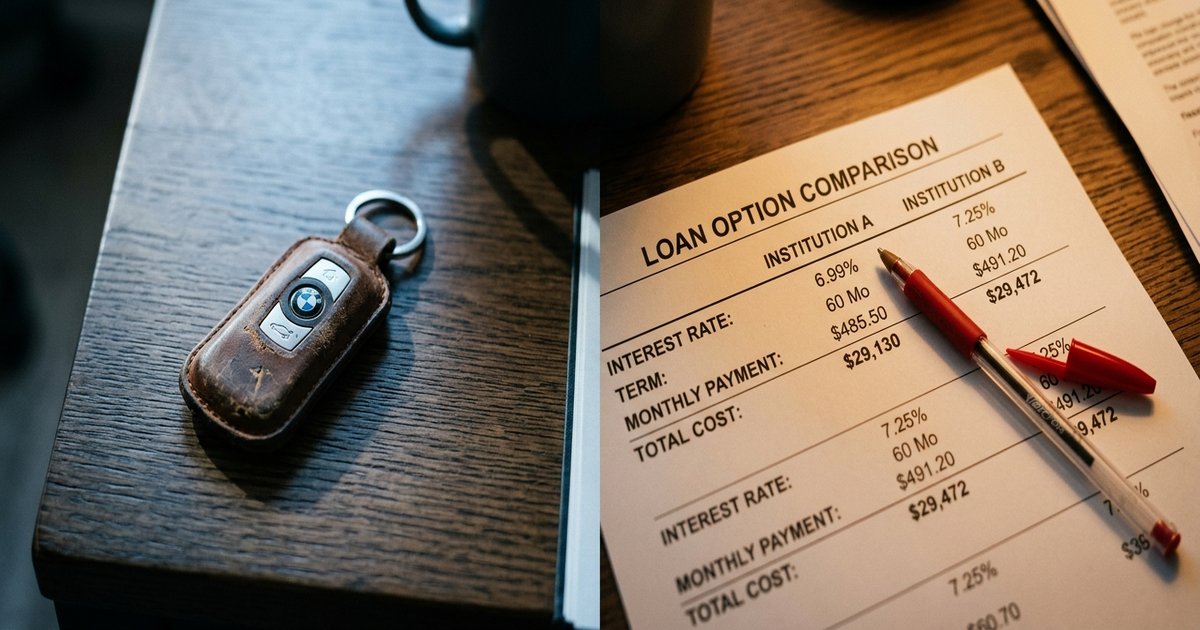

Here's the side-by-side calculation for a $5,000 loan over 36 months. I'm including origination fees because they change the real numbers.

Unsecured option: $5,000 at 28% APR, 4% origination fee ($200 deducted upfront). You receive $4,800 but owe $5,000 plus interest. Monthly payment: approximately $207. Total interest paid: approximately $2,440. Total cost (interest plus origination fee): approximately $2,640.

Secured option (vehicle collateral): $5,000 at 18% APR, 2% origination fee ($100 deducted upfront). You receive $4,900 but owe $5,000 plus interest. Monthly payment: approximately $181. Total interest paid: approximately $1,500. Total cost (interest plus origination fee): approximately $1,600.

Savings from going secured: approximately $1,040 over 36 months.

That's the upside. Now let's look at the downside.

The "Can't Afford to Lose It" Test

Vehicle repossessions surged 43% over two years, reaching 1.73 million in 2024. Projections point to over 3 million repossessions in 2025. Subprime delinquencies (scores 580 to 619) hit a record 6.6% in January 2025, the highest since tracking began in 1994.

Those aren't just numbers. Those are people who pledged their cars, fell behind, and lost their transportation.

Under the Uniform Commercial Code, a lender with a perfected security interest in your vehicle can repossess it without a court order in most states. This is called "self-help repossession." In many cases, they don't need to warn you first. And after the car is sold (usually at auction for well below market value), if the sale doesn't cover your remaining loan balance, the lender can come after you for the difference. That's called a deficiency balance, and many states allow it.

So the worst-case scenario isn't just losing your car. It's losing your car AND still owing money on a loan for a car you no longer have.

Here's the test I'd run before pledging any asset as collateral:

- Is this asset essential to your income? If losing it means you can't get to work, the risk calculation changes fundamentally. Saving $1,040 over three years means nothing if you lose $3,000 a month in wages because you can't commute.

- What's the replacement cost? If your car is worth $8,000, you're risking an $8,000 asset to save $1,040 in interest. The ratio is roughly 8 to 1 against you. If you're securing the loan with a $1,000 CD, you're risking $1,000 to save $1,040. That's a different calculation entirely.

- Do you have a backup? Public transit, a second car, a partner who can drive you, a remote-capable job. If losing the collateral wouldn't strand you, the risk goes down.

- How stable is your income? If you've held the same job for two years and have steady paychecks, the odds of missing payments are lower. If your income is seasonal, gig-based, or unpredictable, every payment is a coin flip, and the risk of repossession climbs.

- Do you have an emergency fund? Even a small one, $500 to $1,000, provides a buffer if a paycheck is late or an expense blindsides you. No emergency fund means one bad month could trigger the repossession chain.

If you answered "yes" to questions 1 and "no" to questions 3, 4, and 5, a secured loan backed by your vehicle is a dangerous bet regardless of the rate savings.

The Safer Collateral Play: Savings and CD-Backed Loans

If the idea of pledging your car makes your stomach knot, there's a middle path that gives you secured-loan rates without the catastrophic downside.

CD-secured loans work like this: you open a certificate of deposit at a credit union or bank, deposit some money (as little as $500 at some institutions), and borrow against it. The CD serves as collateral. The rate drops significantly because the lender's risk is nearly zero. First Tech Federal Credit Union offers these at 6.99% to 18% APR with no origination fee.

The catch: you can't touch the money in the CD until the loan is repaid. It's locked. But you weren't going to spend it anyway, because it's serving as your security deposit. And here's the bonus: your on-time payments get reported to the credit bureaus (OneMain, Upgrade, and most credit union secured lenders report to all three). You're building credit history while borrowing at a lower rate. That's a double benefit.

Self Credit Builder and similar products use this same structure specifically for credit building. You're not borrowing because you need cash. You're borrowing to create a payment history that improves your score over time. If you're focused on that approach, choosing a first bad credit loan strategically explains how to maximize credit-building value.

"I went with a CD-secured loan at my credit union. Put $1,000 in a CD, borrowed against it. Rate was 9%. Best decision I made." That's a real borrower outcome, and it's repeatable.

When Unsecured Is the Smarter Choice (Even at a Higher Rate)

There are situations where paying more in interest is the financially rational decision. That sounds backwards, but it's not.

Your car is your only transportation and you have no backup. If repossession would end your ability to earn income, no interest savings justifies the risk. You're not saving $1,040. You're gambling your livelihood against $1,040.

Your income is unstable. Gig workers, seasonal employees, freelancers with variable months. If your income fluctuates by 30% or more month to month, the probability of a missed payment is too high to pledge a critical asset.

You have no emergency fund. One unexpected expense (car repair, medical bill, family emergency) and you can't make the payment. Without a cushion, secured loans turn routine financial setbacks into asset seizures.

The rate gap is small. If the difference between secured and unsecured is only 3 to 5 percentage points, the total dollar savings over the loan term might be a few hundred dollars. Ask yourself: would you accept a few hundred dollars to let someone put a lien on your car for three years? When the savings are modest, the risk isn't proportional.

You can get a shorter unsecured term. A 24-month unsecured loan at 28% can cost less in total interest than a 48-month secured loan at 20%, simply because you're paying interest for half as long. Always compare total repayment amounts, not just rates. The 7-point loan comparison checklist walks through exactly how to make that calculation.

Title Loans Are Not Secured Personal Loans

I need to make this distinction because the terminology gets blurred, and the consequences of confusing the two are severe.

A secured personal loan from a lender like OneMain Financial or Upgrade has a typical APR of 12% to 36%, a term of 24 to 60 months, and is amortized so every payment chips away at principal and interest.

A title loan from a storefront lender carries an average APR exceeding 300%, with terms of 15 to 30 days. The CFPB has issued multiple warnings about title loans. You hand over your car title, get a fraction of the car's value in cash, and if you can't repay (plus massive interest) in two weeks to a month, you lose the vehicle.

These are completely different products sharing the word "secured." If someone offers you a "secured loan" with a term under 90 days and a rate that feels hard to calculate, you're looking at a title loan. Walk away.

A Quick Checklist Before You Pledge Anything

Run through these seven questions honestly before you commit to a secured loan.

- Is the secured rate at least 8 to 10 percentage points lower than the unsecured rate? (If the gap is smaller, the risk-reward ratio weakens significantly.)

- Is the total dollar savings over the full loan term at least $500? (Smaller savings may not justify the anxiety and risk.)

- Can you afford to lose the collateral without losing your income or your housing?

- Do you have at least one month of loan payments in an emergency fund?

- Has your income been stable for the past 6 months?

- Does the lender report to all three credit bureaus? (If you're putting up collateral, you should be building credit at every bureau.)

- Is the loan term 36 months or less? (Longer secured loans extend your risk exposure window.)

If you answered yes to five or more, a secured loan with appropriate collateral can save you real money. If you answered yes to fewer than four, consider an unsecured loan, a CD-secured alternative, or a different borrowing strategy altogether.

Specific Lenders Worth Comparing

OneMain Financial: APR 11.99% to 35.99%. No minimum credit score. Accepts vehicles under 10 years old. Origination fee 1% to 10% depending on state. Reports to all three credit bureaus. One of the few lenders that works with very low scores and offers both secured and unsecured options so you can compare offers from the same lender.

Upgrade: APR 7.74% to 35.99%. Minimum score 580. Accepts vehicles up to 20 years old. Secured loans may reduce your rate by 1 to 10 percentage points versus unsecured. Origination fee 1.85% to 9.99%. The wider vehicle age acceptance is useful if your car is older.

First Tech Federal Credit Union: APR 6.99% to 18% for savings or CD-secured loans. No origination fee. Loan amounts $500 to $50,000. You need to be a member, but membership is open to most people through a qualifying organization. If you have savings you can pledge, this is one of the most affordable secured options available.

Frequently Asked Questions About Secured vs. Unsecured Bad Credit Loans

What is the average rate difference between secured and unsecured personal loans for bad credit?

The gap typically ranges from 5 to 10 percentage points, though it varies by lender and credit profile. Best Egg reports that their secured rates average about 20% lower than unsecured rates for comparable borrowers. On a $5,000 loan over 36 months, a 10-point rate reduction can save roughly $940 to $1,040 in total interest.

Can a lender repossess my car without warning?

In most states, yes. Under the Uniform Commercial Code, lenders with a perfected security interest can use "self-help repossession" without a court order. Some states require notice before or after repossession, but the rules vary. If you're considering a vehicle-secured loan, check your state's specific repossession laws.

What is a deficiency balance?

If your car is repossessed and sold at auction for less than your remaining loan balance, the difference is called a deficiency balance. Many states allow lenders to pursue you for this amount. So you can lose your car and still owe money on the loan. This is one of the most important risk factors to understand before pledging a vehicle.

Are CD-secured loans available at most banks?

CD-secured loans are primarily offered by credit unions and some community banks. Most large online lenders don't offer them. Availability varies by location, and you'll typically need to be a member of the credit union. Check with local credit unions in your area, as many have open membership criteria.

Is a title loan the same as a secured personal loan?

No. A title loan is a short-term product (15 to 30 days) with APRs often exceeding 300%. A secured personal loan has a multi-year term with APRs typically between 8% and 36%. Title loans are designed as short-term cash advances, and the CFPB has issued multiple warnings about their predatory nature. These are fundamentally different products despite both using a vehicle as security.

Should I use my car as collateral if it's my only transportation?

Only if your income is very stable, you have an emergency fund, and the rate savings are substantial (at least 8 to 10 percentage points lower and at least $500 in total savings over the loan term). If losing the car would cost you your job, the potential savings are dwarfed by the potential income loss. Consider a CD-secured loan or an unsecured loan instead, even at a higher rate.