Every "best bad credit loans" article you've read sorts lenders by APR. Lowest rate at the top, highest at the bottom. Click the affiliate link. Done.

That's fine if you have a 740 credit score and you're comparing 8% to 10%. At those rates, the differences are marginal. But when your score is in the 500s and you're comparing 24% to 32%, the interest rate is only one piece of a much bigger picture. Other factors can cost you more money, wreck your chance to rebuild credit, or trap you in a loan that punishes you for paying it off early.

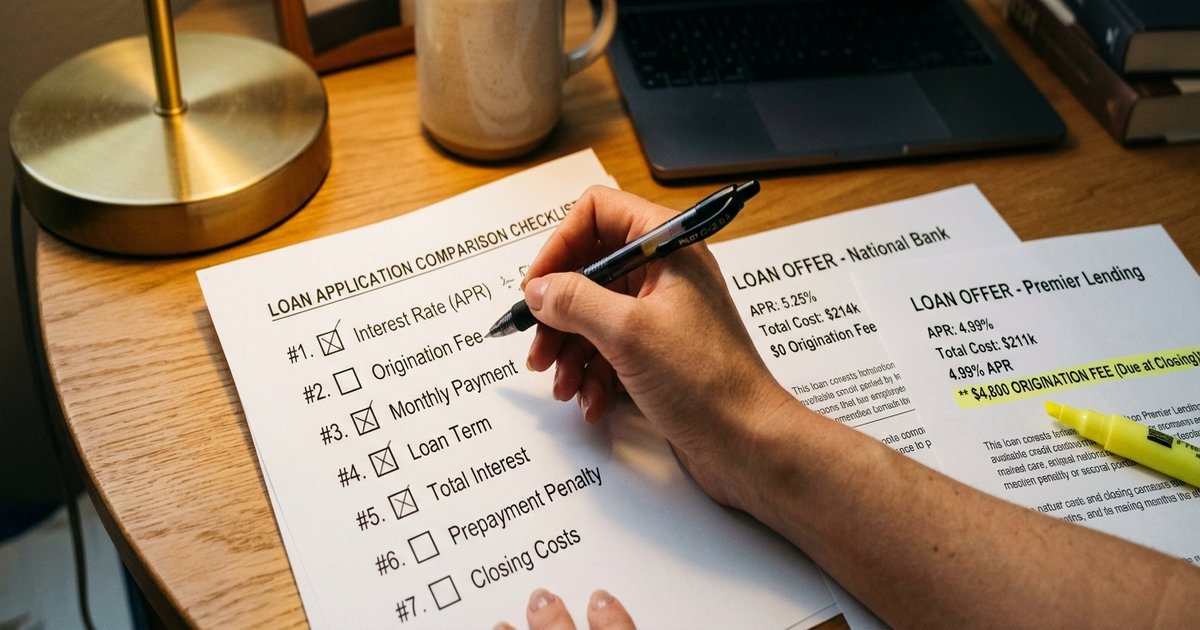

Here are seven criteria I'd check before the rate ever enters the conversation.

Criterion 1: Does the Lender Report to All Three Credit Bureaus?

This is the most overlooked factor in bad credit lending, and it might be the most important one.

When you take out a personal loan and make every payment on time, that payment history should show up on your credit reports. It's one of the few ways to build a positive track record from a bad starting point. But not all lenders report to all three bureaus (Experian, Equifax, TransUnion). Some report to one or two. Some no-credit-check lenders don't report your on-time payments at all.

Here's the painful part: if you default, the debt collector who buys your account almost certainly will report to all three bureaus. So the negative shows up everywhere, but the positive history you worked for? It might show up nowhere, or only on one report.

One borrower put it this way: "I paid every single payment on time for 24 months and my credit score barely moved. Turns out they only reported to one bureau."

Before you sign, ask the lender directly: which credit bureaus do you report to? If they can't give you a straight answer, or if they don't report to all three, that's a meaningful strike against them. You're paying interest on this loan either way. You should be getting credit-building value in return. This is especially important if this is your first bad credit loan, where building a positive tradeline is a primary goal.

Criterion 2: The Origination Fee (What You Actually Receive Versus What You Owe)

Origination fees on bad credit personal loans range from 0% to 15% of the loan amount. The common range is 1% to 10%. That fee gets deducted from your loan disbursement before the money hits your account.

Example: you apply for a $5,000 loan with a 6% origination fee. The lender deducts $300 off the top. You receive $4,700 in your bank account. But you owe $5,000 plus interest. You're paying interest on $300 you never had in your hands.

This is where the advertised APR becomes misleading. Two lenders might both quote you 28% APR, but if one charges a 2% origination fee and the other charges 8%, you're receiving very different amounts of actual money while repaying the same loan balance.

The math you should do: take the loan amount you need, add the origination fee on top, then look at the total repayment on that larger number. If you need $5,000 and the origination fee is 8%, you actually need to borrow around $5,435 to walk away with $5,000 after the fee is deducted. Your interest costs are calculated on that bigger number.

Some lenders, particularly credit unions and certain online lenders, charge zero origination fees. That's not a gimmick. It's real savings that compounds over the life of the loan.

Criterion 3: Soft-Pull Prequalification

A hard credit inquiry drops your score by 5 to 10 points. If you're at 580, losing 10 points puts you at 570. That might not sound catastrophic, but it can push you below a lender's minimum threshold, change your rate tier, or just make your next application harder.

Lenders that offer soft-pull prequalification let you check your estimated rate and terms without any impact on your credit score. You can shop around with three, four, five lenders, compare offers side by side, and only commit to a hard pull when you've identified the best option.

Not all bad credit lenders offer this. Some go straight to a hard pull the moment you submit an application. One borrower learned this the hard way: "They said 'pre-approved' but then did a hard pull and denied me anyway. Now my score is even lower."

Before you apply anywhere, confirm in writing (or on their website) whether the initial check is a soft or hard inquiry. If a lender doesn't offer soft-pull prequalification, they should be lower on your list unless their other terms are significantly better.

Criterion 4: Prepayment Penalties

Say you take out a 36-month loan at 26% APR. Eight months in, you get a tax refund, a bonus, or a small inheritance. You want to pay the loan off early and save yourself 28 months of interest charges.

Some lenders will let you do that with zero penalty. Others will charge you a fee for paying early. This is called a prepayment penalty, and it's designed to protect the lender's expected interest revenue at your expense.

Under the Truth in Lending Act (TILA), lenders are required to disclose prepayment penalties before you sign. But you have to actually read the disclosure. The information is there, buried in the loan agreement, and it matters more than most borrowers realize.

"Read the fine print. My lender charged a prepayment penalty when I tried to pay it off early with my tax refund." That's a real borrower complaint, and it's not rare.

Any lender that charges a prepayment penalty is betting you'll stay in debt for the full term. That's not a lender who's on your side. Cross them off unless there's a compelling reason to stay.

Criterion 5: Funding Speed Versus Total Cost

When you need money for an emergency (car repair, medical bill, past-due rent), speed matters. Some lenders fund the same business day if you apply before their cutoff. Rocket Loans, for example, can fund by the next business day if you apply before 4 PM Eastern. Online lenders generally move faster than traditional banks, which can take 3 to 7 business days.

But speed often comes at a price.

Lenders who market "fast funding" or "same-day approval" to bad credit borrowers tend to charge higher fees and rates. They know you're in a rush, and they price accordingly. The question you need to ask yourself: is the urgency real, or does it just feel urgent?

If your car broke down and you can't get to work without it, same-day funding at a higher cost might be worth it. The math changes if the alternative is losing your income. But if you're consolidating credit card debt or covering a bill that's due in three weeks, you have time to shop around and prioritize total cost over speed. For genuine emergencies, the 72-hour emergency borrowing playbook walks through the fastest options in order of cost.

Don't let a lender's fast-funding marketing rush you into a worse deal than you'd get with 48 hours of patience. And if consolidation is your goal, read why combining bills with bad credit often costs more than keeping your debt separate before you commit.

Criterion 6: Late Payment Policies

Life happens. A paycheck arrives two days late. A direct deposit glitches. You miscalculate your budget one month. What happens when you're a few days late on your loan payment?

The answers vary wildly between lenders, and those differences can cost you hundreds of dollars or torpedo your credit repair efforts.

Questions to ask before signing:

- What's the grace period? Some lenders give you 10 to 15 days after the due date before charging a late fee. Others start the clock immediately.

- What's the late fee? A flat $25 is different from 5% of the missed payment. On a $300 monthly payment, 5% is $15. On a lender that charges a flat $39, you're paying more than double.

- Does one late payment trigger a rate increase? Some lenders have penalty APR clauses. Miss one payment, and your rate jumps. On a 36-month loan, that penalty rate can add hundreds of dollars to your total cost.

- When does the lender report a late payment to the credit bureaus? Federal law says a payment isn't reported as late until it's 30 days past due. But some lenders are faster to report than others. If you're rebuilding credit, one reported late payment can undo months of progress.

Nobody plans to be late. But the borrower with bad credit is statistically more likely to hit a rough patch during the loan term. The lender's policy when things go sideways matters as much as their policy when everything goes right.

Criterion 7: The Total Cost of the Loan

This is the number that actually tells you what the loan costs. Not the APR. Not the monthly payment. The total amount you repay over the full term of the loan, including all interest and fees.

Under TILA, every lender is legally required to disclose this number before you sign. It's called the "total of payments" or "total repayment amount." It's in your loan disclosure documents. Look for it.

Here's why it matters more than APR for bad credit borrowers. A lender might offer you a 24% APR over 60 months. Another offers 28% over 36 months. The first one has a lower rate and a lower monthly payment. Feels like the better deal, right?

Run the numbers on a $5,000 loan. At 24% over 60 months, your total repayment is approximately $8,460. At 28% over 36 months, your total repayment is approximately $7,280. The "higher rate" loan costs you $1,180 less because you're paying it off two years sooner. Monthly payment is higher, but total cost is dramatically lower.

The monthly payment tells you whether you can afford the loan today. The total repayment tells you what the loan actually costs. You need both numbers to make a real comparison.

Your Rights as a Borrower

Federal law gives you specific protections, and in a period when the CFPB has scaled back enforcement (the agency has reduced staff, frozen investigations, and dropped enforcement actions in 2025 and 2026), knowing your rights matters more than it has in years.

Under TILA, lenders must disclose before you sign:

- The loan amount

- The APR

- All finance charges

- Late fees

- Prepayment penalties

- The payment schedule

- The total repayment amount

If any of these are missing from a lender's offer, that's a red flag. If a lender pressures you to sign before providing these disclosures, walk away.

State usury laws also provide protections. Some states cap personal loan APRs at 36%. Others allow significantly higher rates. Check your state attorney general's website for local limits. A rate that's legal in one state might be prohibited in yours. For a detailed breakdown of how state laws affect what you pay as a bad credit borrower, see our state-by-state rankings.

The CFPB received roughly 5.8 million consumer complaints in 2025, with 88% related to credit reporting. If you have a dispute with a lender, you can still file a complaint at consumerfinance.gov, even with reduced enforcement. The complaint creates a public record and often prompts a response from the lender.

The Evaluation Checklist

Use this side by side when comparing loan offers. For each lender, write down the answers. The lender with the most favorable answers across all seven criteria, not just the lowest rate, is your best option.

- Does the lender report on-time payments to all three credit bureaus (Experian, Equifax, TransUnion)?

- What is the origination fee, and what amount will you actually receive after it's deducted?

- Does the lender offer soft-pull prequalification, or does the initial check require a hard inquiry?

- Is there a prepayment penalty if you pay the loan off early?

- How quickly does the lender fund after approval, and what trade-off in cost (if any) comes with faster funding?

- What is the grace period for late payments, the late fee amount, and does a late payment trigger a penalty rate?

- What is the total repayment amount (total of all payments over the full loan term)?

Print this out or save it on your phone. Compare at least three lenders before you commit. The 30 minutes you spend on this checklist can save you hundreds, sometimes thousands, over the life of the loan.

Frequently Asked Questions About Comparing Bad Credit Loans

Why shouldn't I just pick the loan with the lowest APR?

APR doesn't account for origination fees that reduce your actual disbursement, credit bureau reporting practices, prepayment penalties, or the total cost driven by loan term length. A lower APR with a 10% origination fee and a 60-month term can cost far more than a slightly higher APR with no origination fee and a 36-month term. Total repayment amount is a more honest comparison metric.

How do I find out which credit bureaus a lender reports to?

Ask them directly. Check the lender's website FAQ or call their customer service line. If they can't give you a clear answer, consider it a warning sign. Lenders that report to all three bureaus (Experian, Equifax, TransUnion) give you the maximum credit-building benefit for your on-time payments.

What is TILA and how does it protect me?

The Truth in Lending Act is a federal law that requires lenders to disclose the full cost of a loan before you sign, including the APR, finance charges, fees, payment schedule, and total repayment amount. These disclosures are your right, not a favor. If a lender won't provide them upfront, they're violating federal law.

Can I negotiate origination fees?

Some lenders have fixed fee schedules. Others, particularly credit unions, may have flexibility. It's always worth asking. Alternatively, compare lenders that charge zero origination fees. Several online lenders and credit unions offer fee-free personal loans, though other terms may differ.

What happens if the CFPB isn't enforcing consumer protections?

Your legal rights under TILA, FCRA, and ECOA still exist regardless of enforcement levels. You can still file complaints with the CFPB at consumerfinance.gov. State attorneys general also enforce consumer protection laws. And in some cases, private legal action is available for TILA violations. Knowing your rights is your first line of defense, whether or not a federal agency is actively enforcing them.

Is a fast-funding lender always more expensive?

Not always, but frequently. Lenders that market speed to bad credit borrowers often charge higher fees because they know urgency reduces your willingness to shop around. Compare the total repayment amount between a fast-funding lender and a standard-timeline lender. If the difference is small and you genuinely need the money immediately, speed might be worth the premium. If you have a week or two, patience usually pays off.